J. K. Enterprises Vs Superintendent

Date: December 15, 2025

Subject Matter

Writ Petition Challenging Fraudulent ITC Availment Dismissed; Statutory Appellate Remedy Upholds

Summary

The High Court has dismissed a writ petition challenging a Show Cause Notice and Order confirming a demand for fraudulent Input Tax Credit (ITC) availment. The Court found no merit in the petitioner's arguments regarding consolidated SCNs, lack of specific tax amount delineation, non-receipt of personal hearing notices, or jurisdictional issues. Reaffirming the availability of a statutory appellate remedy under Section 107 of the CGST Act, the Court declined to exercise its writ jurisdiction in a case involving large-scale fraudulent ITC availment.

Summary of Facts and Dispute:

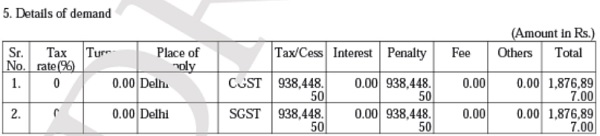

- Impugned Action: Show Cause Notice dated 7th August, 2024, and Order dated 30th January, 2025, were issued by the Superintendent, CGST, Delhi North, confirming a total demand against the Petitioner for fraudulent ITC availment amounting to Rs.13,16,16,906/-, allegedly facilitated by 16 fake firms. The demand for Financial Year 2017-18 was Rs.7,14,322/- and for Financial Year 2018-19 was Rs.11,62,576/-.

- Petitioner's Argument: The Petitioner contended that the impugned SCN and order were impermissible as they related to multiple years without specific delineation of tax amounts, that personal hearing notices were not received, and that the jurisdictional officer lacked the authority to pass the order.

- Core Question of Law: Whether the impugned SCN and order, pertaining to fraudulent ITC availment across multiple financial years, were validly issued and adjudicated, and whether the High Court should exercise its writ jurisdiction despite the availability of a statutory appellate remedy under Section 107 of the CGST Act.

Key Legal Issues & Findings:

Issuance of Consolidated SCN for Multiple Financial Years

The Court relied on its decision in Ambika Traders Through Proprietor Gaurav Gupta V. Additional Commissioner, Adjudication DGGSTI, CGST Delhi North, 2025:DHC:6181-DB, which settled this issue and was subsequently affirmed by the Supreme Court.

- Legislative Intent: Sections 73(3), 73(4), 74(3), and 74(4) of the CGST Act use the terms "for any period" and "for such periods," contrasting with "financial year" used in Sections 73(10) and 74(10), indicating that SCNs can cover periods beyond a single financial year for ITC-related matters.

- Nature of ITC Fraud: Fraudulent ITC utilization often involves connecting transactions across different financial years, making a consolidated SCN necessary to establish a pattern of bogus or fabricated transactions.

Specific Delineation of Tax Amounts for Various Years

The Court examined the record, finding that the DRC-01 form accompanying the impugned SCN clearly specified separate tax amounts for each financial year.

- DRC-01 Clarity: For Financial Year 2017 to 2018, the demand was Rs.7,14,322/-, and for Financial Year 2018 to 2019, the demand was Rs.11,62,576/-, making the petitioner's plea untenable.

Jurisdiction of Adjudicating Officer

The Court referred to Circular No. 31/05/2018-GST dated 9th February, 2018 and subsequent notifications to clarify the jurisdiction in cases involving multiple noticees.

- Multi-Noticee Adjudication: In cases involving multiple noticees, adjudication cannot be performed by each division separately; it must be centralized in one division based on the monetary claims involved and the investigation's progression.

- Highest Demand Principle: The Adjudicating Authority is determined by the jurisdiction having the highest amount of tax demand.

- All India Jurisdiction: Additional/Joint Commissioners of Central Tax with All India jurisdiction can adjudicate SCNs involving multiple noticees, as per Notification No. 02/2022-Central Tax, dated 11th March, 2022, as amended by Notification No. 27/2024-Central Tax, dated 25th November, 2024.

Service of Personal Hearing Notices

The Court reviewed the evidence presented by the department regarding the communication of personal hearing notices.

- Proof of Service: Personal hearing notices dated 14th January, 2025, and 20th January, 2025, were emailed to the petitioner's registered email address (jk_ent85@yahoo.com) on 15th January, 2025, and 21st January, 2025, respectively, as confirmed by GST portal printouts.

- False Plea: The petitioner's claim of non-receipt was deemed false, as the department had complied with service requirements.

Exercise of Writ Jurisdiction in Fraudulent ITC Cases

The Court reiterated its consistent stance, supported by Supreme Court and High Court precedents, against exercising writ jurisdiction in cases of large-scale fraudulent ITC availment. The Court referred to The Assistant Commissioner of State Tax & Ors. v. M/s Commercial Steel Limited, Civil Appeal No. 5121/2021, Mukesh Kumar Garg v. Union of India & Ors., W.P.(C) 5737/2025, M/s Sheetal and Sons & Ors. v. Union of India &Anr., 2025: DHC: 4057-DB, and M/s MHJ Metal Techs v. Central Goods and Services Tax Delhi South, W.P.(C) 5815/2025.

- Extraordinary Remedy: Writ jurisdiction under Article 226 is an extraordinary remedy and should not be exercised when serious allegations of fraudulent ITC availment are involved.

- Statutory Appeal: The availability of an effective statutory appellate remedy under Section 107 of the CGST Act is a strong deterrent to entertaining writ petitions, especially when factual analysis and voluminous evidence are required.

- Burden on Exchequer: Such fraudulent activities jeopardize the GST system, and the balance of convenience lies in protecting the exchequer and the integrity of the GST regime.

Ruling:

- Outcome: The writ petition is dismissed with exemplary costs of Rs.1,00,000/-.

- Directions: The costs of Rs.1,00,000/- shall be paid equally to the Delhi High Court Legal Services Committee and Delhi High Court Bar Association.

- Liberty: The Petitioner is granted liberty to file an appeal under Section 107 of the CGST Act by 15th January, 2026, along with the requisite pre-deposit. If filed within this period, the appeal shall be adjudicated on merits and not be dismissed on the ground of limitation.

FULL TEXT OF THE JUDGMENT/ORDER OF DELHI HIGH COURT

1. This hearing has been done through hybrid mode.

2. The present petition has been filed by the Petitioner through its proprietor Mr. Jai Kishan Bansal under Article 226 of the Constitution of India, inter alia, assailing the impugned Show Cause Notice dated 7th August, 2024 issued by the Superintendent, CGST, Delhi North (hereinafter, ‘impugned SCN’) and the impugned order dated 30th January, 2025 passed by the Superintendent, CGST, Delhi North (hereinafter, ‘impugned order’).

3. Vide the impugned order, the total demand confirmed against the Petitioner is set out below:

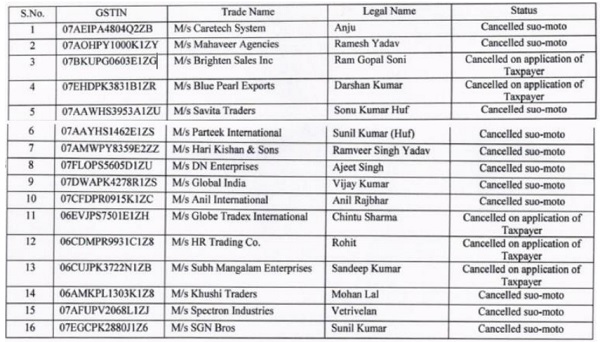

4. The case of the Department is that an investigation was conducted against 575 noticees in the jurisdiction of CGST North who had availed of fake Input Tax Credit (hereinafter, ‘ITC’) totalling to Rs.13,16,16,906/-. The said ITC availment is alleged to have been facilitated by 16 fake firms. The names of the fake firms are as under:

5. The Petitioner is one of the parties who had availed ITC and is shown as a recipient at Sr. No.3 of Table A of the impugned SCN.

6. Thereafter, the common impugned SCN was issued and several recipients of the SCN filed their replies. However, the Petitioner did not file any reply. Personal hearing was also granted to the Petitioner. However, the Petitioner did not attend the same and thereafter, the impugned order has been passed.

7. In support of the filing of the present writ petition, instead of availing of the appellate remedy under Section 107 of the Central Goods and Services Tax Act, 2017 (hereinafter, ‘CGST Act’) the stand of the Petitioner through Mr. Gaurav Gupta, ld. Counsel for the Petitioner is as under:

i. That the impugned SCN and the impugned order relates to multiple years and the same would not be permissible.

ii. That the tax amounts for each of the years are not specifically delineated and separately reflected in the impugned SCN and the impugned order.

iii. That the personal hearing notices were not received by the Petitioner.

iv. That the jurisdictional officer who has passed the impugned order e., the Superintendent, North Range 42, Bawana, Division, did not have the jurisdiction to pass the same.

8. The Court has heard ld. Counsels for the parties. A set of personal hearing notices dated 14th January, 2025 and 20th January, 2025 (hereinafter, ‘personal hearing notices’) have been handed across to the Court.

9. A perusal of the personal hearing notices would show that the personal

hearing notices were emailed to the Petitioner on 15th January, 2025 at 2:49:02 PM on the email address jk_ent85@yahoo.com and on 21st January, 2025 at 4:27:54 PM at jk_ent85@yahoo.com.

10. Additionally, the GST portal print out has also been placed on record to show that this is the registered email address of Mr. Jai Kishan Bansal, the proprietor of the Petitioner, whose mobile no. is 9873256990.

11. Clearly, the filing of the present writ petition is without any basis. The Petitioner had a duty to reply to the impugned SCN as the investigation which was conducted by the Department was well within the knowledge of the Petitioner.

12. Further, even after passing of the impugned order, the present writ petition was listed on 30th May, 2025 which is the last day when the three plus one month limitation period, in terms of Section 107(4) of the CGST Act.

Issue of Consolidated SCN

13. Moreover, insofar as the issuance of consolidated SCN for multiple financial years is concerned, the said issue stands settled by this Court in the decision in Ambika Traders Through Proprietor Gaurav Gupta V. Additional Commissioner, Adjudication DGGSTI, CGST Delhi North, 2025:DHC:6181-DB. The relevant portion of the said decision reads as under:

“Consolidated SCN for Multiple Financial Years

43. Insofar as the issue of consolidated notice for various financial years is concerned, a perusal of Section 74 of the CGST Act would itself show that at least insofar as fraudulently availed or utilized ITC is concerned, the language used in Section 74(3) of the CGST Act and Section 74(4) of the CGST Act is “for any period” and “for such periods” respectively. This contemplates that a notice can be issued for a period which could be more than one financial year. Similar is the language even in Section 73 of the CGST Act. The relevant provisions read as under:

“73. Determination of tax [, pertaining to the period up to Financial Year 2023-24,] not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised for any reason other than fraud or any wilful-misstatement or suppression of facts.––

XXXX

(3) Where a notice has been issued for any period under sub-section (1), the proper officer may serve a statement, containing the details of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised for such periods other than those covered under sub-section (1), on the person chargeable with tax.

(4) The service of such statement shall be deemed to be service of notice on such person under subsection (1), subject to the condition that the grounds relied upon for such tax periods other than those covered under sub-section (1) are the same as are mentioned in the earlier notice.

XXXX

74. Determination of tax [, pertaining to the period up to Financial Year 2023-24,] not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised by reason of fraud or any wilful misstatement or suppression of facts.––

XXXX

(3) Where a notice has been issued for any period under sub-section (1), the proper officer may serve a statement, containing the details of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised for such periods other than those covered under sub-section (1), on the person chargeable with tax.

(4) The service of statement under sub-section (3) shall be deemed to be service of notice under subsection (1) of section 73, subject to the condition that the grounds relied upon in the said statement, except the ground of fraud, or any wilful-misstatement or suppression of facts to evade tax, for periods other than those covered under subsection (1) are the same as are mentioned in the earlier notice.”

44. Some of the other provisions of the CGST Act, which are relevant, include Section 2(106) of the CGST Act, which defines “tax period” as under

“2.[…] (106) “tax period” means the period for which the return is required to be furnished”

45. Thus, Sections 74(3), 74(4), 73(3) and 73(4) of the CGST Act use the term “for any period” and “for such periods”. This would be in contrast with the language used in Sections 73(10) and 74(10) of the CGST Act where the term “financial year” is used. The said provisions read as under:

“73.[…] (10) The proper officer shall issue the order under sub-section (9) within three years from the due date for furnishing of annual return for the financial year to which the tax not paid or short paid or input tax credit wrongly availed or utilised relates to or within three years from the date of erroneous refund”

“74.[…] 10) The proper officer shall issue the order under sub-section (9) within a period of five years from the due date for furnishing of annual return for the financial year to which the tax not paid or short paid or input tax credit wrongly availed or utilised relates to or within five years from the date of erroneous refund.”

The Legislature is thus, conscious of the fact that insofar as wrongfully availed ITC is concerned, the notice can relate to a period and need not to be for a specific financial year.

46. The nature of ITC is such that fraudulent utilization and availment of the same cannot be established on most occasions without connecting transactions over different financial years. The purchase could be shown in one financial year and the supply may be shown in the next financial year. It is only when either are found to be fabricated or the firms are found to be fake that the maze of transactions can be analysed and established as being fraudulent or bogus.

47. A solitary availment or utilization of ITC in one financial year may actually not be capable of by itself establishing the pattern of fraudulent availment or utilization. It is only when the series of transactions are analysed, investigated, and enquired into, and a consistent pattern is established, that the fraudulent availment and utilization of ITC may be revealed. The language in the abovementioned provisions i.e., the word `period’ or `periods’ as against `financial year’ or `assessment year’ are therefore, significant.”

14. The SLP against the decision in Ambika Traders Through Proprietor Gaurav Gupta (Supra) was also dismissed as withdrawn. The relevant portion of the said order dated 1st September, 2025 in SLP(C) No. 023774/2025 reads as under:

“1. After arguing the matter for some time, the learned counsel appearing for the petitioner states that he does not want to press this petition.

2. The petition is accordingly dismissed as not pressed”

Thus, the issue in respect of issuance of a consolidated SCN for multiple years stands settled.

Issue of Separate Tax amounts for various years

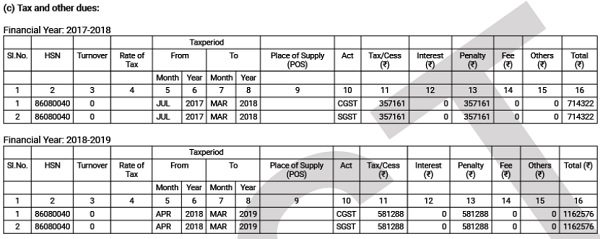

15. Insofar as the reflection of the tax amounts for the various years are concerned, the DRC-01 which was accompanying the impugned SCN itself specifically gives all amounts for all the years separately in the following terms:

16. A perusal of the same would show that, for Financial Year 2017 to 2018, the demand is Rs.7,14,322/- and Financial Year 2018 to 19, the demand is Rs. 11,62,576/-. Thus, the aforesaid plea is also completely untenable.

Issue of Jurisdiction

17. Insofar as the issue in respect of jurisdiction of Superintendent, North Range 42, Bawana, Division, is concerned, Mr. Shashank Sharma, ld. Counsel for the Respondent has explained that firstly, a substantial number of noticees are in the said Commissionerate. Secondly, when there are more than 575 noticees who are involved, the notice cannot be adjudicated by each and every division separately as applicable to their respective parties. The adjudication has to take place in one Division based upon the monetary claims involved which are monetary demands in the said Division.

18. This Court is of the opinion that in cases involving multiple noticees, the adjudication cannot be done by different commissioner rates and the commissionerate is decided, depending upon the monetary demands that are proposed to be raised and the manner in which the investigation would have proceeded. Circular No. 31/05/2018-GST dated 9th February, 2018 is relevant in this regard. The relevant portion of the circular reads as under:

“5. Whereas, for optimal distribution of work relating to the issuance of show cause notices and orders under sections 73 and 74 of the CGST Act and also under the IGST Act, monetary limits for different levels of officers of central tax need to be prescribed. Therefore, in pursuance of clause (91) of section 2 of the CGST Act read with section 20 of the IGST Act, the Board hereby assigns the officers mentioned in Column (2) of the Table below, the functions as the proper officers in relation to issue of show cause notices and orders under sections 73 and 74 of the CGST Act and section 20 of the IGST Act (read with sections 73 and 74 of the CGST Act), up to the monetary limits as mentioned in columns (3), (4) and (5) respectively of the Table below:-

| Sl. No. | Officer of Central tax | Monetary limit of the amount of central tax (including cess) not paid or short paid or erroneously refunded or input tax credit of central tax wrongly availed or utilized for issuance of show cause notices and passing of orders under sections 73 and 74 of CGST Act. |

Monetary limit of the amount of integrated tax (including cess) not paid or short paid or erroneously refunded or input tax credit of integrated tax wrongly availed or utilized for issuance of show cause notices and passing of orders under sections 73 and 74 of CGST Act made applicable to matters in relation to integrated tax vide section 20 of the IGST Act |

Monetary limit of the amount of central tax and integrated tax (including cess) not paid or short paid or erroneously refunded or input tax credit of central tax and integrated tax wrongly availed or utilized for issuance of show cause notices and passing of orders under sections 73 and 74 of CGST Act made applicable to integrated tax vide section 20 of the IGST Act |

| 1. | Superintendent of Central Tax | Not exceeding Rupees 10 lakhs | Not exceeding Rupees 20 lakhs | Not exceeding Rupees 20 lakhs |

| 2. | Deputy or Assistant Commissioner of Central Tax | Above Rupees 10 lakhs and not exceeding Rupees 1 crore |

Above Rupees 20 lakhs and not exceeding Rupees 2 crores |

Above Rupees 20 lakhs and not exceeding 2 crores |

| 3. | Additional or Joint Commissioner of Central Tax | Above Rupees 1 crore without any limit | Above Rupees 2 crores without any limit | Above Rupees 2 crores without any limit |

6. The Central Tax officers of Audit Commissionerates and Directorate General of Goods and Services Tax Intelligence (hereinafter referred to as “DGGI”) shall exercise the powers only to issue show cause notices. A show cause notice issued by them shall be adjudicated by the competent Central Tax officer of the executive Commissionerate in whose jurisdiction the noticee is registered when such cases pertain to jurisdiction of one executive Commissionerate of Central Tax only.

7.1 In respect of show-cause notices issued by officers of DGGI, there may be cases where,

i. a show cause-notice is issued to multiple noticees, either having the same or different PANs; or

ii. multiple show cause-notices are issued on the same issue to multiple noticees having the same PAN,

and the principal place of business of such noticees fall under the jurisdiction of multiple Central Tax Commissionerates. For the purpose of adjudication of such show cause notices, Additional/Joint Commissioners of Central Tax of specified Commissionerates have been empowered with All India jurisdiction through amendment in the Notification No. 02/2027, dated 19th June, 2017 vide Notification No. 02/2022-Central Tax, dated 11th March, 2022, as further amended vide Notification No. 27/2024-Central Tax, dated 25th November, 2024. Such show cause- notices may be adjudicated, irrespective of the amount involved in the show cause-notice(s), by one of the Additional/Joint Commissioners of Central Tax empowered with All India jurisdiction vide the above mentioned notifications. Principal Commissioners/ Commissioners of the Central Tax Commissionerates specified in the said notification will allocate charge of Adjudication (DGGI cases) to one or more Additional Commissioners/ Joint Commissioners posted in their Commissionerates. Where the location of principal place of business of the noticee, having the highest amount of demand of tax in the said show cause-notice(s), falls under the jurisdiction of a Central Tax Zone/Commissionerate mentioned in column 2 of the table below, the show cause-notice(s) may be adjudicated by one of the Additional Commissioners/ Joint Commissioners of Central Tax, holding the charge of Adjudication (DGGI cases), of the Central Tax Commissionerate mentioned in column 3 of the said table corresponding to the said Central Tax Zone/Commissionerate. Such show cause notice(s) may, accordingly, be made answerable by the officers of DGGI to the concerned Additional/ Joint Commissioners of Central Tax”.

19. From the above, it is clear that when there are multiple parties involved and Show Cause Notices have to be adjudicated, the Adjudicating Authority is fixed on the basis of the jurisdiction which has the highest amount of demand tax.

20. Furthermore, this Court takes serious note of the fact that the stand of the Petitioner was that the personal hearing notices were not received. Once the email has been sent at the registered email ad dress, the compliance has been affected by the Department. The emails which have been placed on record leave no manner of doubt in the mind of the Court that the personal hearing notices were in fact served upon the Petitioner. The plea that the notices were not served is, therefore, a false plea.

Cases involving fraudulent availment of ITC

21. Finally, this Court takes serious note of the fact in cases involving such a large scale fraudulent availment of ITC, the entire GST system itself is being jeopardized by such parties as the Petitioner. The repeated number of cases where such fraudulent availment ITC is seen, raises a serious concern as to the manner in which a benefit which was meant to be utilised by businesses is being misused by illegal methods.

22. This Court has consistently taken the view that in cases involving fraudulent availment of ITC, ordinarily, the Court would not be inclined to exercise its writ jurisdiction. It is routinely seen in such cases that there are complex transactions involved which require factual analysis and consideration of voluminous evidence, as also the detailed orders passed after investigation by the Department. In such cases, it would be necessary to consider the burden on the exchequer as also the nature of impact on the GST regime, and balance the same against the interest of the Petitioner, which is secured by availing the right to statutory appeal.

23. It would be relevant to refer to some of the cases which have been decided by the Supreme Court as also by this Court on these aspects. The Supreme Court in the context of CGST Act, has, in Civil Appeal No. 5121/2021 dated 3rd September, 2021 titled ‘The Assistant Commissioner of State Tax & Ors. v. M/s Commercial Steel Limited’, has held as under:

“11. The respondent had a statutory remedy under section 107. Instead of availing of the remedy, the respondent instituted a petition under Article 226. The existence of an alternate remedy is not an absolute bar to the maintainability of a writ petition under Article 226 of the Constitution. But a writ petition can be entertained in exceptional circumstances where there is: (i) a breach of fundamental rights; (ii) a violation of the principles of natural justice; (iii) an excess of jurisdiction; or (iv) a challenge to the vires of the statute or delegated legislation.

12. In the present case, none of the above exceptions was established. There was, in fact, no violation of the principles of natural justice since a notice was served on the person in charge of the conveyance. In this backdrop, it was not appropriate for the High Court to entertain a writ petition. The assessment of facts would have to be carried out by the appellate authority. As a matter of fact, the High Court has while doing this exercise proceeded on the basis of surmises. However, since we are inclined to relegate the respondent to the pursuit of the alternate statutory remedy under Section 107, this Court makes no observation on the merits of the case of the respondent.

13. For the above reasons, we allow the appeal and set aside the impugned order of the High Court. The writ petition filed by the respondent shall stand dismissed. However, this shall not preclude the respondent from taking recourse to appropriate remedies which are available in terms of Section 107 of the CGST Act to pursue the grievance in regard to the action which has been adopted by the state in the present case”

24. Thereafter, this Court in W.P.(C) 5737/2025 titled Mukesh Kumar Garg v. Union of India & Ors. dealing with a similar case involving fraudulent availment of ITC had held as under:

“11. The Court has considered the matter under Article 226 of the Constitution of India, which is an exercise of extraordinary writ jurisdiction. The allegations against the Petitioner in the impugned order are extremely serious in nature. They reveal the complex maze of transactions, which are alleged to have been carried out between various non-existent firms for the sake of enabling fraudulent availment of the ITC.

12. The entire concept of Input Tax Credit, as recognized under Section 16 of the CGST Act is for enabling businesses to get input tax on the goods and services which are manufactured/supplied by them in the chain of business transactions. The same is meant as an incentive for businesses who need not pay taxes on the inputs, which have already been taxed at the source itself. The said facility, which was introduced under Section 16 of the CGST Act is a major feature of the GST regime, which is business friendly and is meant to enable ease of doing business.

13. It is observed by this Court in a large number of writ petitions that this facility under Section 16 of the CGST Act has been misused by various individuals, firms, entities and companies to avail of ITC even when the output tax is not deposited or when the entities or individuals who had to deposit the output tax are themselves found to be not existent. Such misuse, if permitted to continue, would create an enormous dent in the GST regime itself.

14. As is seen in the present case, the Petitioner and his other family members are alleged to have incorporated or floated various firms and businesses only for the purposes of availing ITC without there being any supply of goods or services. The impugned order in question dated 30th January, 2025, which is under challenge, is a detailed order which consists of various facts as per the Department, which resulted in the imposition of demands and penalties. The demands and penalties have been imposed on a large number of firms and individuals, who were connected in the entire maze and not just the Petitioner.

15. The impugned order is an appealable order under Section 107 of the CGST Act. One of the co-noticees, who is also the son of the Petitioner i.e. Mr. Anuj Garg, has already appealed before the Appellate Authority. 16. Insofar as exercise of writ jurisdiction itself is concerned, it is the settled position that this jurisdiction ought not be exercised by the Court to support the unscrupulous litigants.

17. Moreover, when such transactions are entered into, a factual analysis would be required to be undertaken and the same cannot be decided in writ jurisdiction. The Court, in exercise of its writ jurisdiction, cannot adjudicate upon or ascertain the factual aspects pertaining to what was the role played by the Petitioner, whether the penalty imposed is justified or not, whether the same requires to be reduced proportionately in terms of the invoices raised by the Petitioner under his firm or whether penalty is liable to be imposed under Section 122(1) and Section 122(3) of the CGST Act.

18. The persons, who are involved in such transactions, cannot be allowed to try different remedies before different forums, inasmuch as the same would also result in multiplicity of litigation and could also lead to contradictory findings of different Forums, Tribunals and Courts.”

25. This position was also followed in M/s Sheetal and Sons & Ors. v. Union of India &Anr., 2025: DHC: 4057-DB. The relevant portion of the said decision read as under:

“15. The Supreme Court in the decision in Civil Appeal No 5121 of 2021 titled ‘The Assistant Commissioner of State Tax & Ors. v. M/s Commercial Steel Limited’ discussed the maintainability of a writ petition under Article226. In the said decision, the Supreme Court iterated the position that existence of an alternative remedy is not absolute bar to the maintainability of a writ petition, however, a writ petition under Article 226 can only be filed under exceptional circumstances….

XXXX

16. In view of the fact that the impugned order is an appealable order and the principles laid down in the abovementioned decision i.e. The Assistant Commissioner of State Tax & Ors. (Supra), the Petitioners are relegated to avail of the appellate remedy.”

26. Recently, this Court in W.P.(C) 5815/2025 titled M/s MHJ Metal Techs v. Central Goods and Services Tax Delhi South held as under:

“16. This Court, while deciding the above stated matter, has held that where cases involving fraudulent availment of ITC are concerned, considering the burden on the exchequer and the nature of impact on the GST regime, writ jurisdiction ought not to be exercised in such cases. The relevant portions of the said judgment are set out below:

“11. The Court has considered the matter under Article 226 of the Constitution of India, which is an exercise of extraordinary writ jurisdiction. The allegations against the Petitioner in the impugned order are extremely serious in nature. They reveal the complex maze of transactions, which are alleged to have been carried out between various non-existent firms for the sake of enabling fraudulent availment of the ITC.

12. The entire concept of Input Tax Credit, as recognized under Section 16 of the CGST Act is for enabling businesses to get input tax on the goods and services which are manufactured/supplied by them in the chain of business transactions. The same is meant as an incentive for businesses who need not pay taxes on the inputs, which have already been taxed at the source itself. The said facility, which was introduced under Section 16 of the CGST Act is a major feature of the GST regime, which is business friendly and is meant to enable ease of doing business.

13. It is observed by this Court in a large number of writ petitions that this facility under Section 16 of the CGST Act has been misused by various individuals, firms, entities and companies to avail of ITC even when the output tax is not deposited or when the entities or individuals who had to deposit the output tax are themselves found to be not existent. Such misuse, if permitted to continue, would create an enormous dent in the GST regime itself.

14. As is seen in the present case, the Petitioner and his other family members are alleged to have incorporated or floated various firms and businesses only for the purposes of availing ITC without there being any supply of goods or services. The impugned order in question dated 30th January, 2025, which is under challenge, is a detailed order which consists of various facts as per the Department, which resulted in the imposition of demands and penalties. The demands and penalties have been imposed on a large number of firms and individuals, who were connected in the entire maze and not just the Petitioner.

15. The impugned order is an appealable order under Section 107 of the CGST Act. One of the co-noticees, who is also the son of the Petitioner i.e. Mr. Anuj Garg, has already appealed before the Appellate Authority.

16. Insofar as exercise of writ jurisdiction itself is concerned, it is the settled position that this jurisdiction ought not be exercised by the Court to support the unscrupulous litigants.

17. Moreover, when such transactions are entered into, a factual analysis would be required to be undertaken and the same cannot be decided in writ jurisdiction. The Court, in exercise of its writ jurisdiction, cannot adjudicate upon or ascertain the factual aspects pertaining to what was the role played by the Petitioner, whether the penalty imposed is justified or not, whether the same requires to be reduced proportionately in terms of the invoices raised by the Petitioner under his firm or whether penalty is liable to be imposed under Section 122(1) and Section 122(3) of the CGST Act.

18. The persons, who are involved in such transactions, cannot be allowed to try different remedies before different forums, inasmuch as the same would also result in multiplicity of litigation and could also lead to contradictory findings of different Forums, Tribunals and ”

17. Under these circumstances, this Court is not inclined to entertain the present writ petition. However, the Petitioners are granted the liberty to file an appeal.

18. Accordingly, the Petitioners are permitted to avail of the appellate remedy under Section 107 of the CGST Act, by 15th July, 2025, along with the necessary pre-deposit mandated, in which case the appeal shall be adjudicated on merits and shall not be dismissed on the ground of limitation.

19. Needless to add, any observations made by this Court would not have any impact on the final adjudication by the appellate authority.”

27. The decision in Metal Techs (Supra) has also been carried to the Supreme Court in SLP(C) 27411/2025 titled M/S Metal Techs v. Central Goods and Services Tax Delhi South. In the said SLP, the Supreme Court vide order dated 22nd September, 2025 has merely extended the time for filing the appeal.

28. Under these circumstances, this Court is not inclined to entertain the present petition and in fact all the grounds raised in the petition are also devoid of any merit.

29. The Petitioner is also guilty of concealing material facts relating to service of communications from the department for personal hearings etc., The writ petition is dismissed with exemplary costs of Rs.1,00,000/-. The costs shall be paid divided equally to the Delhi High Court Legal Services Committee and Delhi High Court Bar Association.

30. The bank account details are as follows:

(i) Delhi High Court Bar Association – Rs.50,000/-

-

- Name: Delhi High Court Bar Association

- Account No.: 15530100000478

- IFSC: UCBA0001553

- Bank & Branch: UCO Bank, Delhi High Court

- Name: Delhi High Court Bar Association

- Account No.: 15530100000478

- IFSC: UCBA0001553

- Bank & Branch: UCO Bank, Delhi High Court

(ii) Delhi High Court Legal Services Committee: – Rs.50,000/-

-

- Name: Delhi High Court Legal Services Committee

- Account No.: 15530110008386

- Bank & Branch : UCO Bank, Delhi High Court

- IFSC: UCBA0001553

- Name: Delhi High Court Legal Services Committee

- Account No.: 15530110008386

- Bank & Branch : UCO Bank, Delhi High Court

- IFSC: UCBA0001553

31. On the request of ld. Counsel for the Petitioner, considering this as an exceptional case where the Petition was first listed when the last date of the limitation was expiring, the Court is inclined to permit the Petitioner to avail of the appellate remedy in accordance with law, in terms of Section 107 of the CGST Act.

32. If the appeal is filed by 15th January, 2026, along with the requisite pre-deposit, the same shall be adjudicated on merits and not be dismissed on the ground of limitation.

33. The present petition is disposed of in these terms. Pending applications, if any, are also disposed of.